Are you wondering if your shiny new car will cost more to insure? You’re not alone.

Many people like you are curious about the factors that affect car insurance rates for new vehicles. Understanding these factors can help you make informed decisions and possibly save money. We’ll dive into the reasons why insurance for new cars can be pricier and what you can do about it.

Stick with us, and by the end, you’ll have a clearer picture of how to navigate your car insurance options effectively.

Factors Affecting New Car Insurance Costs

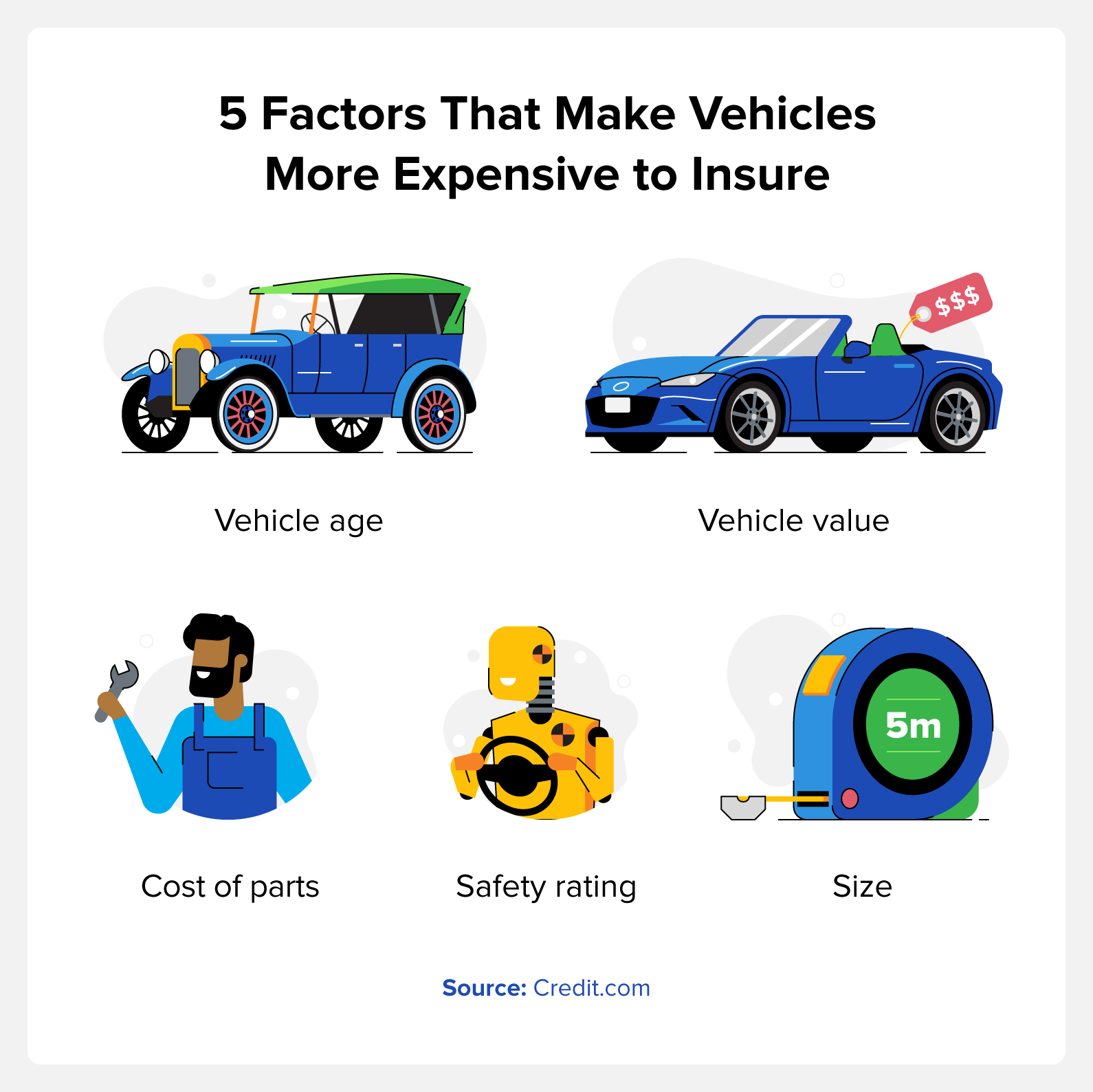

Several factors influence the cost of insuring a new car. Insurance companies assess risks based on different vehicle characteristics. Understanding these factors helps explain why insurance premiums vary for new cars.

Vehicle Value And Repair Costs

New cars usually have higher market values. Insurers consider the car’s worth when setting premiums. Repair parts for new models may cost more. Complex designs can increase repair time and expenses. Higher repair costs lead to higher insurance rates.

Advanced Safety Features

Many new cars come with modern safety technology. Features like automatic braking and lane assist can reduce accident chances. Insurers may offer discounts for these systems. However, repairing high-tech equipment can be costly. The balance between safety benefits and repair costs affects premiums.

Theft Risk And Security Systems

New cars may attract thieves more than older ones. Insurance companies check theft statistics for specific models. Cars with strong security systems get lower rates. Alarms, GPS tracking, and immobilizers help prevent theft. These features reduce insurance costs by lowering risk.

)

Credit: insurify.com

Comparison Between New And Used Car Insurance

Understanding the differences between insuring a new car versus a used one can help you make smarter decisions about your coverage and budget. Insurance costs vary based on several factors tied to the car’s age and value. Let’s break down how premiums, coverage needs, and depreciation affect your insurance for new and used vehicles.

Premium Differences

New cars usually come with higher insurance premiums than used cars. This happens because new vehicles have a higher market value and cost more to repair or replace after damage.

For example, if you buy a brand-new SUV, the insurer expects higher repair bills for parts and labor, which pushes your premium up. On the other hand, a five-year-old car often costs less to insure since its value has dropped and repairs may be cheaper.

But don’t assume every new car will break your bank. Some models have lower repair costs or come with safety features that insurers reward with discounts. Have you checked how your preferred car’s safety ratings impact your premium?

Coverage Requirements

New cars often require more comprehensive coverage than used cars. Lenders may demand full coverage if you’re financing your vehicle, which includes collision and comprehensive insurance.

Used cars, especially those owned outright, might only need liability insurance to meet legal requirements. This reduces your monthly cost but also lowers your protection level.

Consider your risk tolerance. Are you willing to pay more upfront to protect a new car fully? Or do you prefer minimal coverage on an older car that’s less valuable but more prone to breakdowns?

Depreciation Impact

Depreciation hits new cars hardest in the first few years, significantly lowering their value. Insurance companies factor this in when determining payouts for total loss claims.

For a new car, the payout might cover most of your purchase price early on. But as depreciation sets in, used cars will have lower payout amounts, meaning you might need to cover the difference out of pocket.

This can influence whether you choose gap insurance—a type of coverage that pays the difference between what you owe on your car and its depreciated value. Is gap insurance worth the extra cost for your new car?

Tips To Lower Insurance For New Cars

Lowering insurance costs for new cars helps manage your budget better. New cars often cost more to insure due to their high value and repair costs. Small changes in your insurance plan can save you money. Focus on smart choices and good habits to reduce premiums.

Choosing The Right Coverage

Pick coverage that fits your needs and budget. Avoid paying for extras you do not need. Consider liability, collision, and comprehensive coverage carefully. Higher deductibles can lower your premium but mean more cost if you claim. Review your policy yearly to adjust coverage as your car ages.

Discounts And Incentives

Insurance companies offer many discounts that can cut costs. Common discounts include:

- Good driver discounts

- Multi-policy discounts for bundling home and auto insurance

- Low mileage discounts if you drive less

- Safety feature discounts for cars with airbags or alarms

Ask your insurer about all available discounts before buying a policy.

Maintaining A Clean Driving Record

Safe driving lowers insurance costs over time. Avoid tickets, accidents, and claims. Insurance companies reward drivers with fewer claims. Use defensive driving courses to improve skills and reduce rates. Consistency in safe driving habits is key to keeping premiums low.

Credit: www.k923orlando.com

Credit: credit.com

Frequently Asked Questions

Is Car Insurance Costlier For New Cars?

Yes, car insurance tends to be more expensive for new cars. New vehicles have higher repair costs and greater market value. Insurers consider these factors when setting premiums, making coverage for new cars pricier than for older models.

Why Do New Cars Have Higher Insurance Premiums?

New cars have higher premiums due to their higher replacement costs. Advanced safety features and technology also increase repair expenses. Insurers factor in the vehicle’s value and repair complexity, leading to higher insurance costs for new cars.

Can I Reduce Insurance On My New Car?

Yes, you can lower insurance costs by increasing deductibles or bundling policies. Installing safety devices and maintaining a clean driving record also help. Comparing quotes from different insurers ensures you get the best premium for your new car.

Does Car Model Affect New Car Insurance Rates?

Absolutely, the car model significantly impacts insurance rates. Luxury and sports cars usually cost more to insure due to higher repair costs. Safer, more common models often have lower premiums, even if they are new.

Conclusion

New cars often cost more to insure than older ones. They have higher repair and replacement costs. Safety features can lower rates, but value and theft risk matter more. Choosing the right coverage helps control expenses. Shopping around can find better deals.

Understanding your car insurance helps you make smart decisions. Keep these points in mind for your next car purchase. Insurance costs vary, so stay informed and prepared.